Fed Officials Signal Pause in Rates, Dollar Retreats

- Dollar loses steam after Fed members indicate ‘pause’ in rate hikes

- US debt ceiling deal passes House, but stocks and gold uninterested

- Eurozone inflation data and key US releases coming up next

Fed officials kneecap dollar

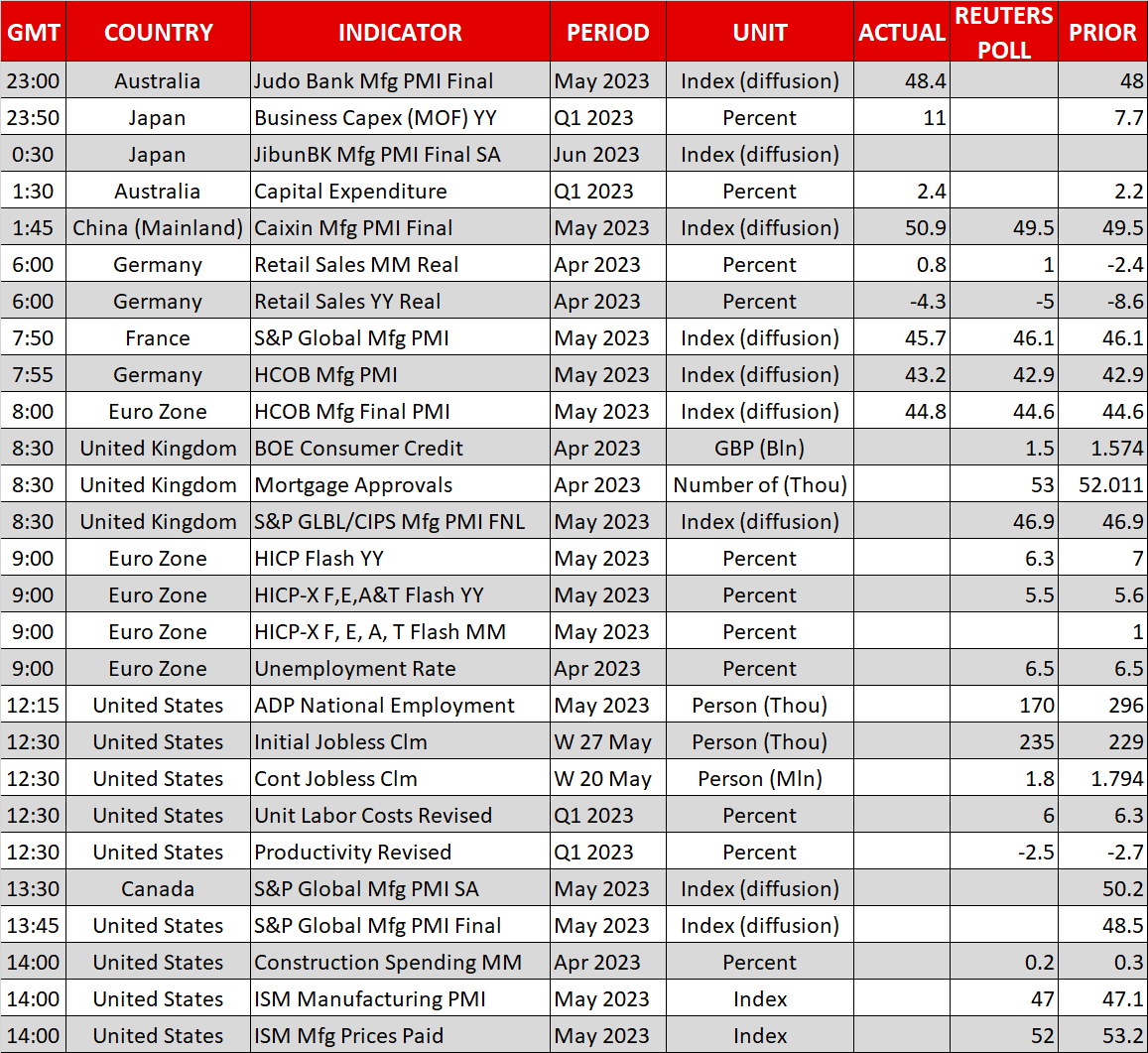

Bets that the Federal Reserve will raise interest rates this month receded yesterday, after a couple of FOMC members signaled they would rather “skip” a rate increase. Fed Board Governor Jefferson, who is also the nominee for vice-chair, joined forces with Philly Fed President Harker to telegraph a potential pause in the tightening cycle.

Both of them stressed that skipping a rate increase this month does not necessarily mean interest rates have peaked for this cycle. It would simply allow policymakers extra time to examine incoming data before making any decisions, effectively keeping the door wide open for another hike in July.

These cautious remarks knocked the wind out of the US dollar, which was flying high earlier in the session following some encouraging JOLTS employment data. The probability that the Fed will raise rates in June fell to 38% in the aftermath from almost 70% previously, dragging US yields lower.

Looking ahead, with Fed officials and investors split on whether another rate increase is on the menu in two weeks, there will be increased emphasis on economic data to settle the debate. The show will kick off today with the ISM manufacturing survey and the ADP jobs print, which will serve as appetizers for tomorrow’s official employment report.

US debt ceiling deal passes House

In the political sphere, the House of Representatives overwhelmingly approved the deal to raise the debt ceiling in a 314-117 vote yesterday, dispelling fears of a government default. The bill will now head to the Senate, before President Biden can sign it into law.

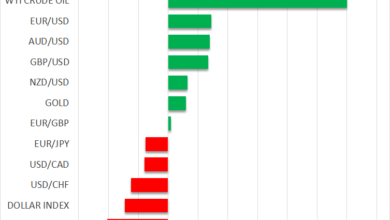

Markets did not react much, as the passage of this bill is seen as a formality at this stage. Gold was little changed near the $1,955 zone, kept afloat by the Fed-induced pullback in the dollar and yields. In the near-term, the yellow metal’s fortunes are linked to whether the FOMC will raise rates this month.

Stock markets declined yesterday, with the S&P 500 losing 0.6% of its value to fall back below the crucial 4,200 region. It seems that the astonishing rally in tech stocks has started to fatigue and things could get dicier over the summer in an environment of tighter liquidity conditions, expensive valuations, and stagnant earnings growth.

Euro eyes inflation stats

In the euro area, the latest inflation stats will hit the markets today. Estimates suggest core inflation cooled only marginally in May, but most of the country-level reports so far have come in way below forecasts, posing some downside risks.

A surprisingly soft inflation report could push back against market bets that the ECB will raise interest rates another two times this summer, keeping the euro under selling pressure. From a chart perspective, the ‘line in the sand’ for euro/dollar is the 1.0520 area, where a downside violation would mark a lower low and signal that the longer-term uptrend is no longer in play.

Finally in the US, traders will keep a close eye on the ISM index amid growing signs that the manufacturing sector globally is losing steam. Meanwhile, the ADP employment report will give investors a sense of what to expect from tomorrow’s nonfarm payrolls, driving the dollar accordingly.