Natural Gas in $2 Death Grip as Storage Rampage Continues

NG

+0.04%

Add to/Remove from Watchlist

Add to Watchlist

Add Position

Position added successfully to:

Please name your holdings portfolio

Type:

BUY

SELL

Date:

Amount:

Price

Point Value:

Leverage:

1:1

1:10

1:25

1:50

1:100

1:200

1:400

1:500

1:1000

Commission:

Create New Watchlist

Create

Create a new holdings portfolio

Add

Create

+ Add another position

Close

- Natural gas market is seeing a surplus in storage, with inventories 33% above year-ago levels and 20% higher than the five-year average.

- The projected 74 bcf addition to gas storage would lift stockpiles to 2.137 trillion cubic feet, or tcf, for the week ended May 5 — 31% above the same week a year ago and about 18% above the five-year average.

- Mild spring weather, low gas demand, maintenance on pipelines, and a drop in exports of liquefied natural gas have driven spot prices of natural gas to negative territory this week.

Storage. Storage. Storage.

The natural gas market just can’t seem to get enough of storage.

With gas inventories from two weeks ago already 33% above year-ago levels and 20% higher than the five-year average, last week’s forecast addition of 74 billion cubic feet or bcf — which are just marginally lower historically — won’t do much for longs in the game wishing to escape the $2 price trap.

The latest weekly gas build will be verified by the US Energy Information in an update due at 10:30 AM ET (14:30 GMT) today.

It comes after another round of barely supportive weather — for the gas market that is, though Americans would love the perfect not-too-cold, not-too-warm temperatures.

Just a fortnight ago, there were real chills that triggered some indoor heating. But all that dissipated after rains in recent days, and weak wind conditions that could not carry any coolness across the country.

Said Houston-based energy markets advisory Gelber & Associates in a note on natural gas:

“Precipitation and a low pressure system rolling through Texas currently have cooled the warmer temperatures that have materialized as of late reducing some of the necessary cooling demand.”

For a precise reading, heat data from Reuters-associated data provider Refinitiv showed there were around 62 heating degree days, or HDDs, last week compared with a 30-year normal of 47 HDDs for the period.

HDDs measure the number of degrees a day’s average temperature is below 65 degrees Fahrenheit (18 degrees Celsius) to estimate demand to heat homes and businesses.

The projected 74 bcf addition to gas storage last week would lift stockpiles to 2.137 trillion cubic feet, or tcf, for the week ended May 5. That would be 31% above the same week a year ago and about 18% above the five-year average — an improvement from the prior week but, as emphasized earlier, just marginally.

Gelber’s analysts said in their note that US gas output remains slightly below the recent peak of 101 bcf per day, providing a little relief to longs in the space — though that would not be long.

“[Output] is expected to return [higher] after maintenance [at production sites] ends,” the note said.

Offsetting any meaningful impact from the lower output was a drop in exports of liquefied natural gas, or LNG, Gelber’s analysts said, adding:

“All of this points to hefty storage injections in the coming weeks in the 100s.”

Mild spring weather, low gas demand, and maintenance on pipelines had already driven spot, or cash, prices of natural gas to negative territory at the West Texas Waha hub this week.

In Wednesday’s trading, Waha prices closed at -$0.35 per million metric British thermal units.

It was the first time spot prices had settled in negative territory since October 2020. There were sessions this past October where Waha hub traded in the negative, but those sessions closed in positive territory.

The Waha hub’s unusual dynamics — where there is a lot of supply but not enough takeaway capacity — combined with maintenance works and low gas demand put Waha in this position.

Analysts are of the opinion that even after maintenance concludes and demand regularizes, the Waha hub will return to normal pricing but remaining at a significant discount to gas futures on the Henry Hub.

At the time of writing, Henry Hub’s front month, June, hovered at just under $2.20 per mmBtu — caught in the death grip of middling $2 levels that have been the mainstay of gas futures since February. Notwithstanding the relative stability of the futures market, Henry Hub’s front month is down more than 50% on the year since the start of the year. Natural Gas Daily Chart

Natural Gas Daily Chart

Charts indicate little immediate change in the fortunes of June gas, said Sunil Kumar Dixit, chief technical strategist at SKCharting.com.

“A daily and weekly close above $2.40 will be initial signs of a resumption of the uptrend in Henry Hub’s front month, to be affirmed by a clearing through of the swing high of $2.55,” Dixit said.

Beyond that, sits the longer-term target of 100-day Simple Moving Average, he said, adding:

“The flip side is that a steady dip beneath the 5-day Exponential Moving Average, or EMA of $2.19, will keep the downside momentum going. That could invite potential drops to $2.04 and $1.94.”

LNG Marching to Own Drummer

On the LNG front, a halting restart to production at Freeport LNG has lifted basis prices somewhat in the East Texas gas market this month, S&P Global Commodity Insights said in a report this week.

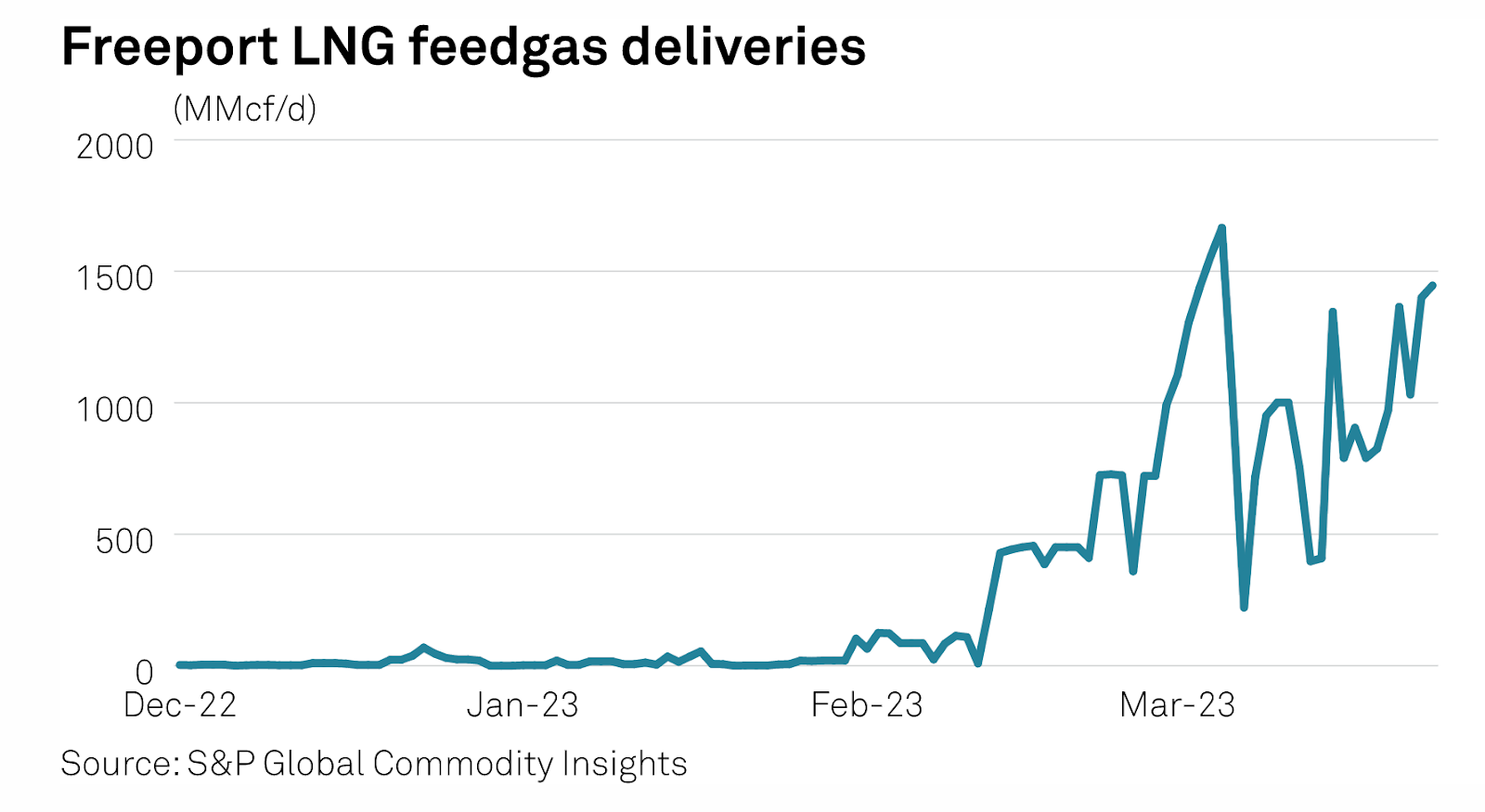

In March, gas deliveries to the Quintana Island liquefaction plant averaged just over 1.0 bcf per day.

But flows to the terminal have swung significantly, ranging from as high as nearly 1.7 bcf/d on March 5 to as low as about 220 million metric cubic feet per day, or mmcf/d, on March 7, S&P data showed. Freeport LGN Feedgas Deliveries

Freeport LGN Feedgas Deliveries

Freeport was on track to receive more than 1.4 bcf/d of feedgas on March 24 after topping 1.0 bcf/d for the previous three days, based on evening cycle nomination data that could later be revised.

The return of Freeport from an eight-month-long outage has helped lift overall US LNG feedgas deliveries, which are now on pace for a new monthly average high of nearly 13.1 bcf/d through March 24.

That’s a figure that’s on track to top the historical monthly record of 12.8 bcf/d set in March 2022. Market participants are watching the ramp-up of operations at Freeport as a factor that could bolster languishing Gulf Coast gas prices as it tightens regional market fundamentals.

On the Henry Hub, futures have so far largely shrugged off the restart of feedgas demand at Freeport.

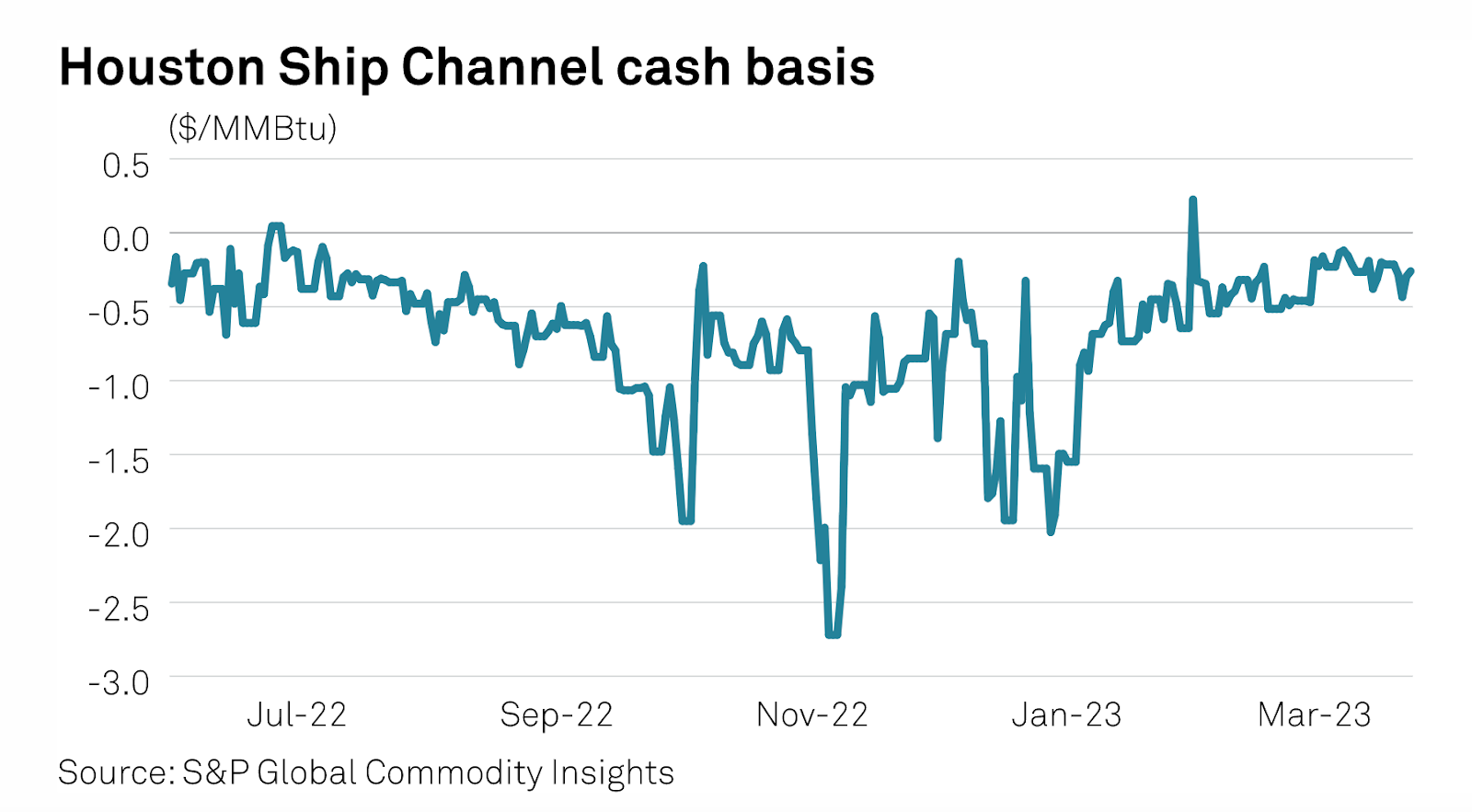

But on the East Texas gas market, though, additional feedgas demand from Freeport has undoubtedly tightened the supply-demand balance. At Houston Ship Channel, cash prices have strengthened to an average 24 cents discount to Henry Hub this month – up from a 42 cents discount in February and 67 cents discount in January, Platts data shows.

During the extended outage at Freeport, basis prices at Houston Ship Channel and Katy Hub experienced wild swings, trading on more than several occasions at discounts of $2 per mmBtu or more to Henry Hub. In the months prior to the terminal’s shutdown, basis prices at the two East Texas hubs only averaged about 25 cents discount to the US benchmark. Houston Ship Channel Cash Basis

Houston Ship Channel Cash Basis

At the same time, the effort at Freeport LNG to return to full service appears to be “skewing pipeline samples out of the Haynesville shale and creating a distorted view of natural gas supply trends,” East Daley Analytics said in a recent research note.

East Daley cited pipeline flows in East Texas and northern Louisiana that appeared to trail off at the end of February from an all-time high, prompting speculation that Haynesville producers could be shutting in wells in response to lower gas prices.

Instead, the analysts said they believe gas at the Carthage hub, a key trading point for Haynesville supply, was being redirected south onto intrastate pipelines to meet Freeport LNG feedgas demand, rather than being shipped east to northeastern Louisiana.

On Feb. 21, US regulators gave Freeport LNG a greenlight to resume production at its first two trains, followed just over two weeks later by an authorization on March 8 to begin operating its third train.

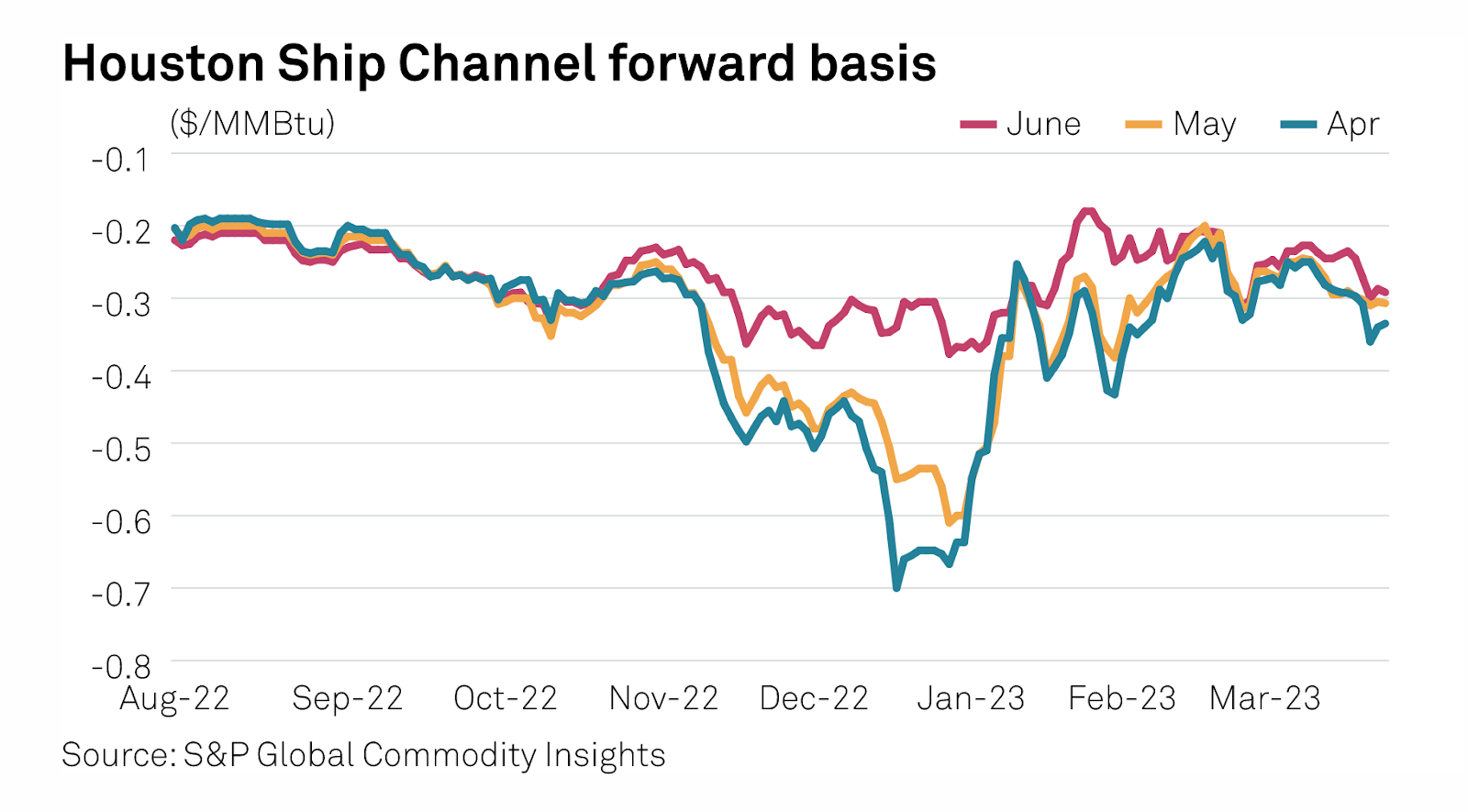

Based on earlier restart projections from Freeport, many traders may have assumed that a regulatory go-ahead would have been followed by a quick ramp-up in feedgas flows to Freeport – back to pre-outage levels of around 2 bcf/d. Houston Ship Channel Forward Basis

Houston Ship Channel Forward Basis

Last month, forward basis markets at Houston Ship Channel appeared to foresee that outcome.

In mid-February, the East Texas hub’s April and May forward contracts both strengthened to about 20 cents behind the corresponding Henry Hub forward price. As of late March, though, the forward market spread has widened with April and May now trading about 32 cents behind Henry Hub as the market takes stock of the stumbling restart at Freeport.

S&P Global forecasts that US LNG feedgas demand will average 13.4 bcf/d in 2023, up from 11.8 bcf/d last year. The forecast sees LNG feedgas rising as it heads into winter 2023-24, peaking at 14 bcf/d in November.

Globally, the resumption of LNG production at Freeport is expected to be the single-largest supply addition to the international LNG market in 2023.

Ramping operations underway at the facility will also help determine the overall strength of US LNG feedgas demand exiting winter.

“The spring shoulder season is often when US facilities take liquefaction units offline for seasonal maintenance – potentially compounding the market impact of continued weakness in feedgas demand at Freeport,” S&P Global said.

The forecaster also reported hearing four cargoes from Freeport LNG canceled in March as the operator experienced valve issues on Train 1 and electrical issues on Train 2, according to market sources. Freeport, however, declined to comment.

***

Disclaimer: